![[Report] The Alternative Lending Opportunity in South East Asia](/insights/content/images/2021/05/underbanked.jpeg)

This ADDX Insights Report is part of an ongoing series exploring opportunities in private markets and alternative investments. This report was produced by Lightstream Research and was commissioned by ADDX.

Executive Summary

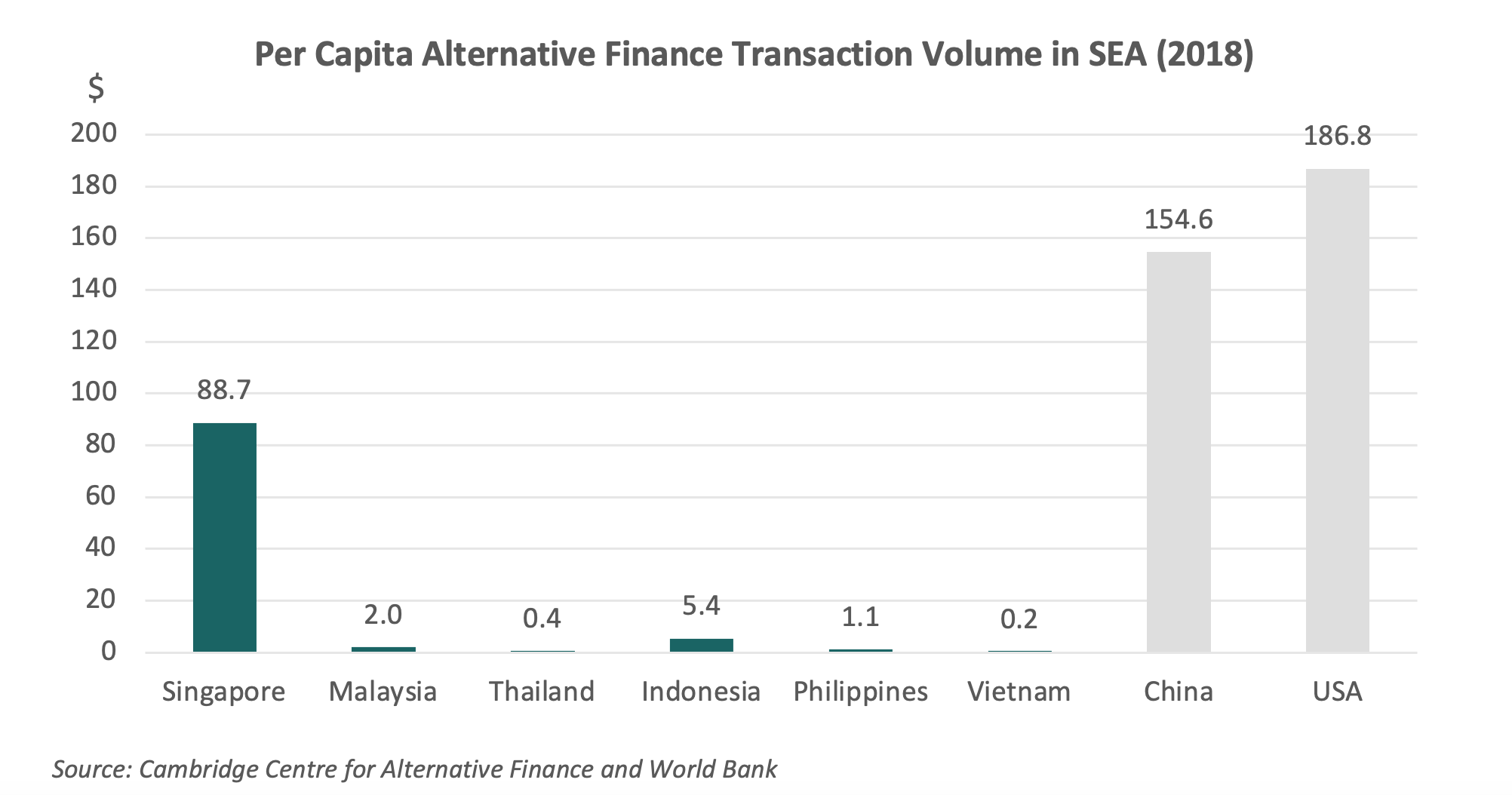

The alternative finance market in South East Asia (SEA) is relatively under-penetrated, accounting for less than 1% of global transaction volume. Indonesia, despite being the largest alternative finance market in the region, has a per capita alternative finance transaction volume of only $5 compared to $155 and $187 respectively in China and the USA. The penetration is even lower in other SEA markets, except in Singapore, where business lending takes precedence.

Despite the relatively low penetration, there is a significant opportunity for the alternative lending industry in the SEA region, particularly in markets such as Indonesia, the Philippines, and Vietnam. Strong growth in consumer spending coupled with relatively low banking penetration and the tendency to borrow from informal sources bode well for the alternative lending industry in these markets. There is also a significant opportunity for the alternative lending industry to bridge the financing gap for SMEs in the region. SMEs are a big part of SEA economies accounting for around 30%-50% of GDP; however, poor access to finance is one of the top issues for SMEs in the region.

Singapore and Indonesia are the only SEA countries that currently have specific regulatory frameworks for the alternative lending industry. However, more than 80% of the alternative financing platforms in Singapore, the Philippines, and Malaysia believe that regulations are adequate and appropriate. The regulatory environment in Indonesia seems somewhat restrictive given that only around 64% of the alternative financing platforms deem that the regulations are favourable.

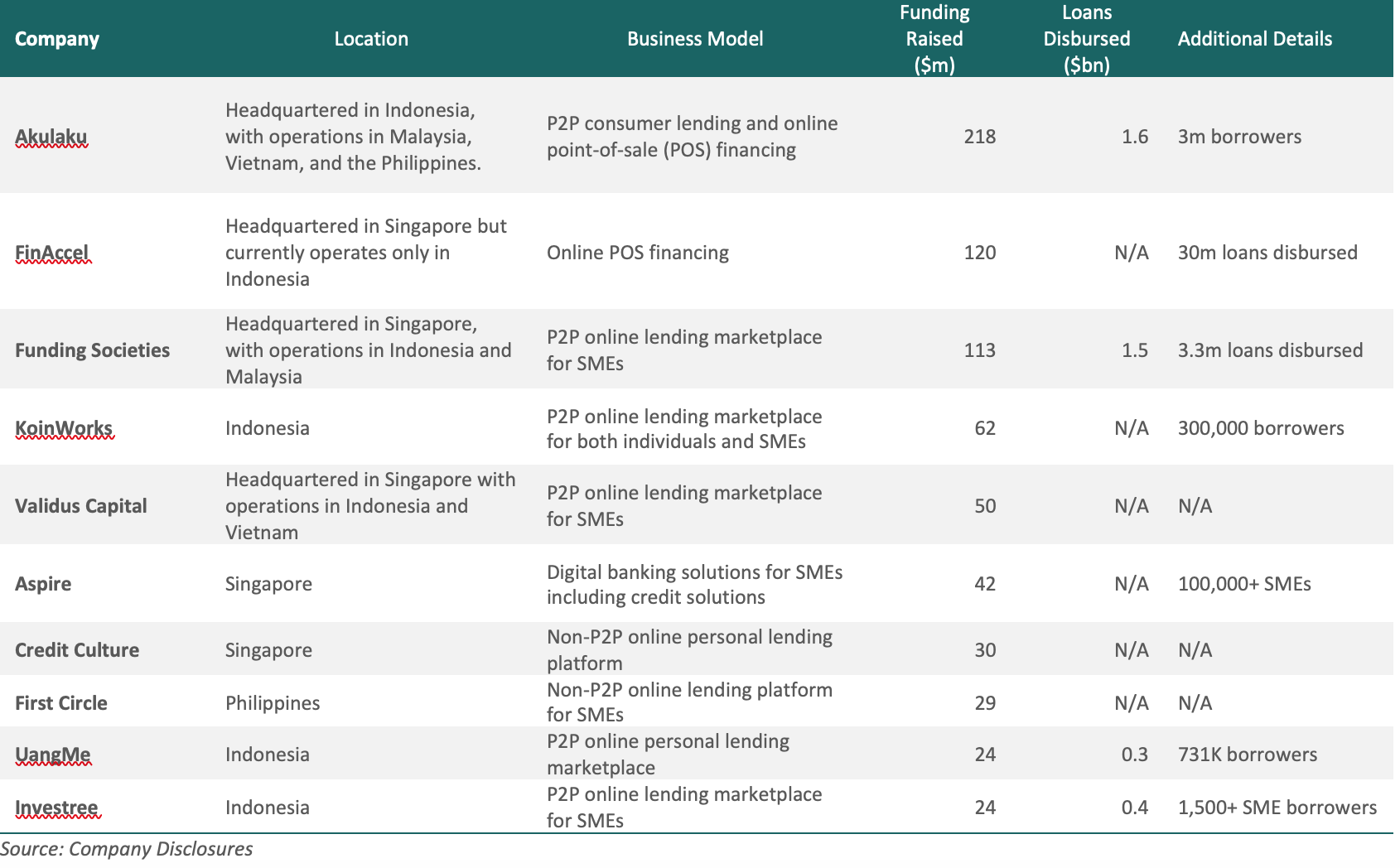

The alternative lending market in SEA is highly fragmented with the presence of a large number of small players. Nevertheless, a few notable established players also exist. Akulaku (Indonesia), FinAccel (Singapore), and Funding Societies (Singapore) are the largest alternative lending companies in the region in terms of funds raised.

Indonesia and Singapore stand out, but market dynamics are vastly different from each other

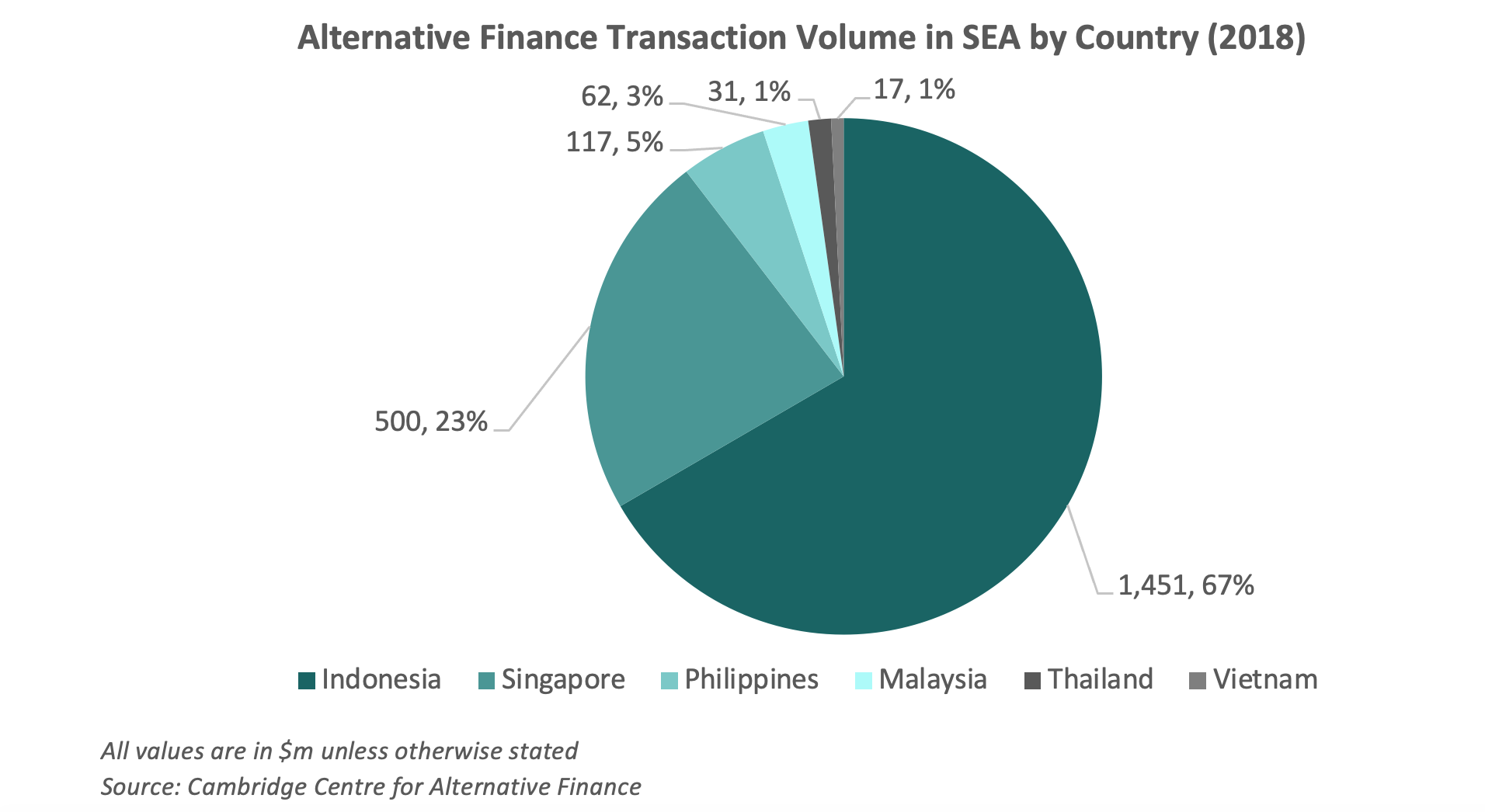

The alternative finance market in South East Asia (SEA) facilitated around $2.2bn in transaction volume in 2018 (including both fintech lending and fintech equity transactions such as equity crowdfunding). This was around 0.7% of the global alternative finance transaction volume and 2.5% of the global alternative finance transaction volume excluding China (China accounts for around 70% of global alternative finance transaction volume).

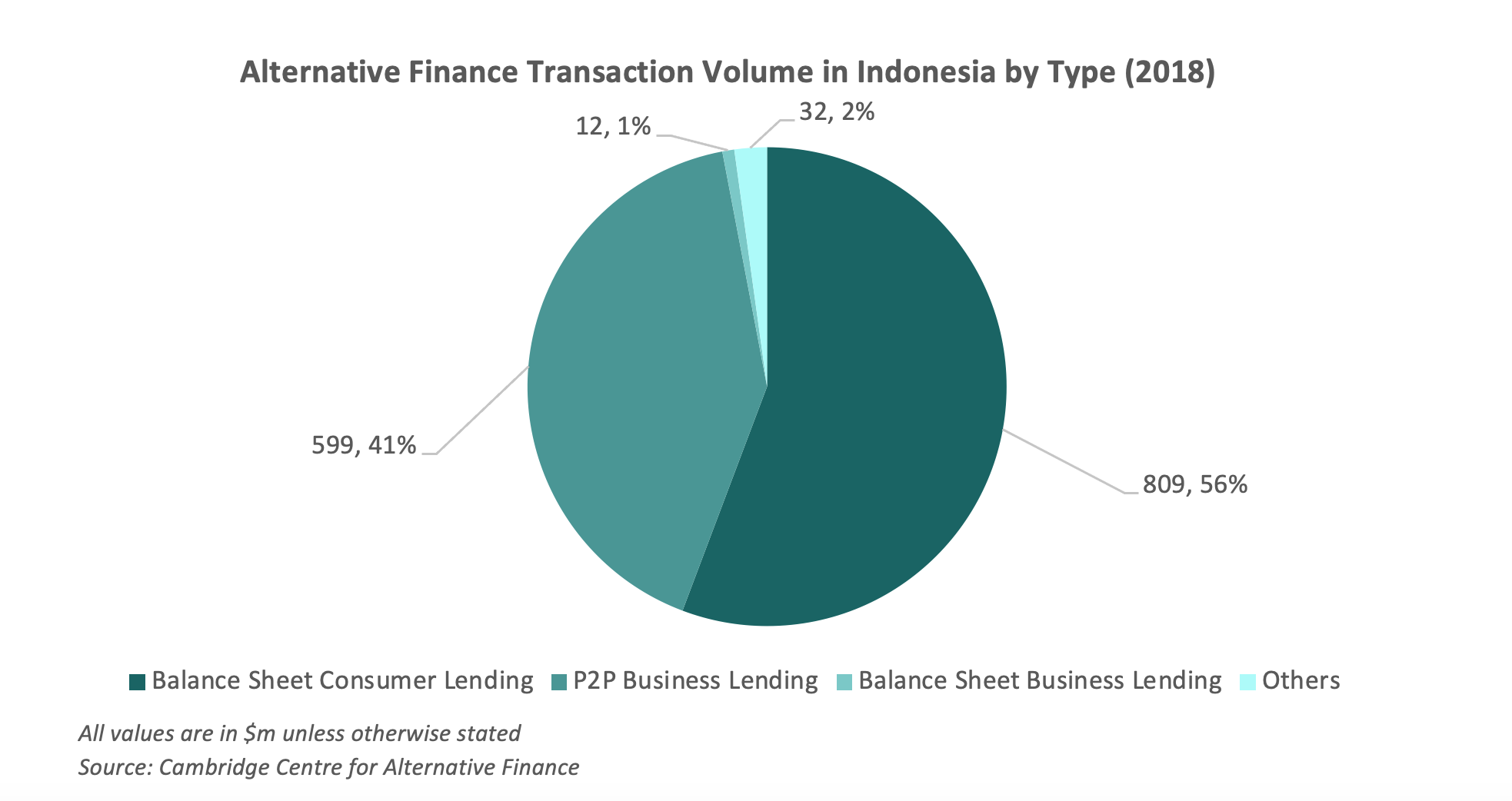

Indonesia is the largest alternative finance market in SEA with a transaction volume of $1.5bn, followed by Singapore ($500m) and the Philippines ($117m). Indonesia is also the fifth largest alternative finance market in the world (behind China, the US, the UK, and the Netherlands). The alternative finance market in Indonesia is driven by balance sheet consumer lending (or in other words, non-P2P consumer lending), which accounts for around 57% of the total transaction volume. Indonesia is also the largest non-P2P consumer alternative lending market in the Asia-Pacific region.

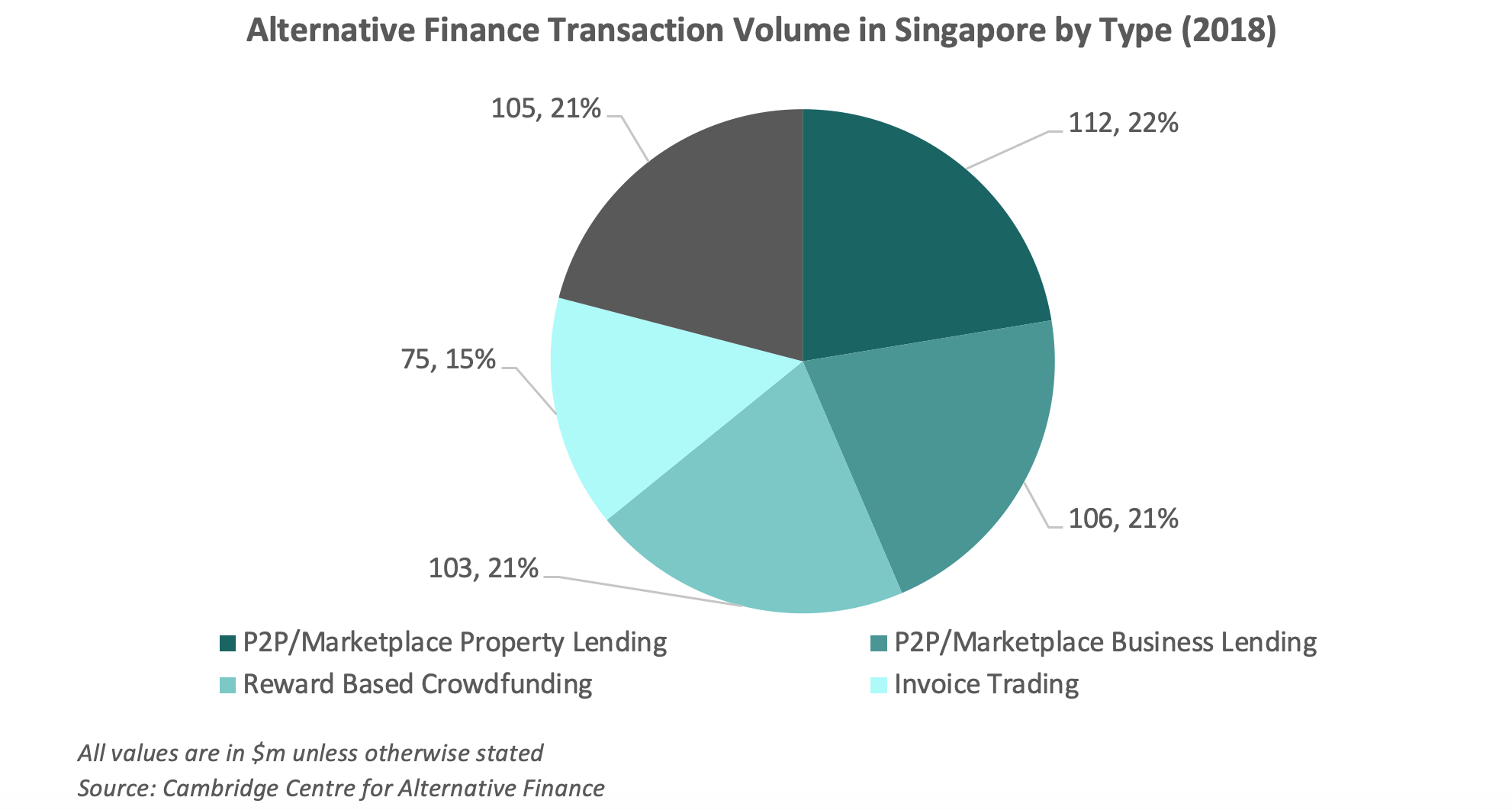

Singapore’s alternative finance market is driven by business lending, which accounts for more than 80% of the country’s alternative finance transaction volume. This is a marked difference compared to the rest of SEA, where personal lending takes precedence. Alternative financing is popular among SMEs that cannot secure loans from traditional financial institutions. The most popular forms of alternative SME financing in Singapore are P2P lending and reward-based crowdfunding. Singapore is the largest reward-based crowdfunding market and the third-largest P2P business lending market in the Asia-Pacific region

The Philippines is also another relatively large alternative finance market in SEA. The alternative finance market in the Philippines is driven by non-P2P consumer lending, which accounts for around 40% of the country’s alternative finance transaction volume. Apart from Indonesia, Singapore, and the Philippines, alternative financing operations in other SEA markets are still relatively small.

Despite robust growth in recent years, SEA markets are still heavily under-penetrated

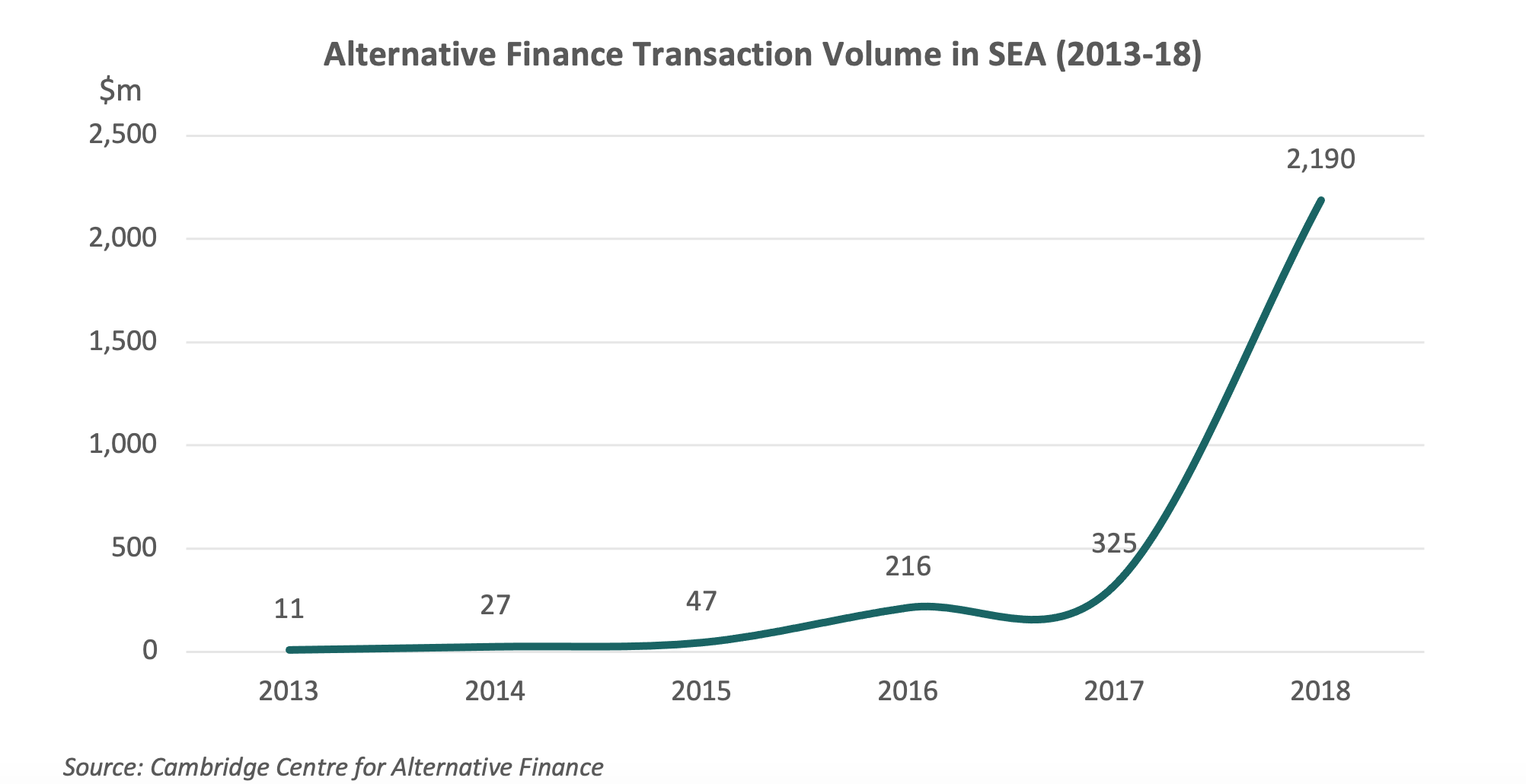

The alternative finance transaction volume in SEA increased at a robust 3-year CAGR of 361% over 2015-18. Indonesia and Singapore contributed to around 68% and 21% of this growth respectively. The total contribution to growth from other markets was less than 10% during this period.

The alternative finance transaction volume in Indonesia increased by 129% YoY and 1714% YoY respectively in 2017 and 2018. However, despite this strong growth, the alternative finance market in Indonesia is still heavily under-penetrated. Indonesia’s per capita alternative finance transaction volume is around $5, compared to $155 and $187 respectively in China and the USA. The penetration is even lower in other SEA markets (except in Singapore, due to the prominence of business lending).

Low access to credit in Indonesia and the Philippines bodes well for alternative consumer lending

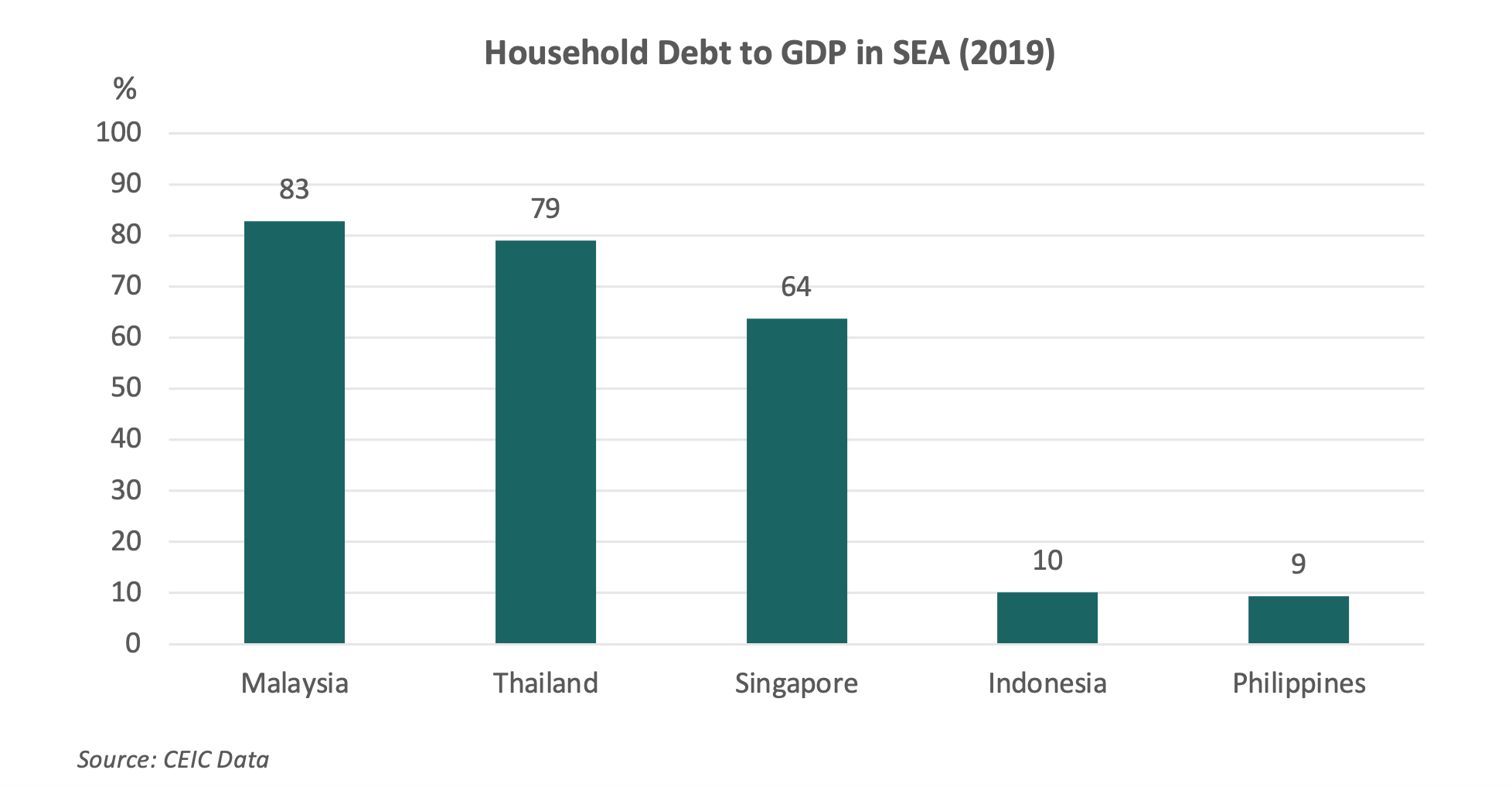

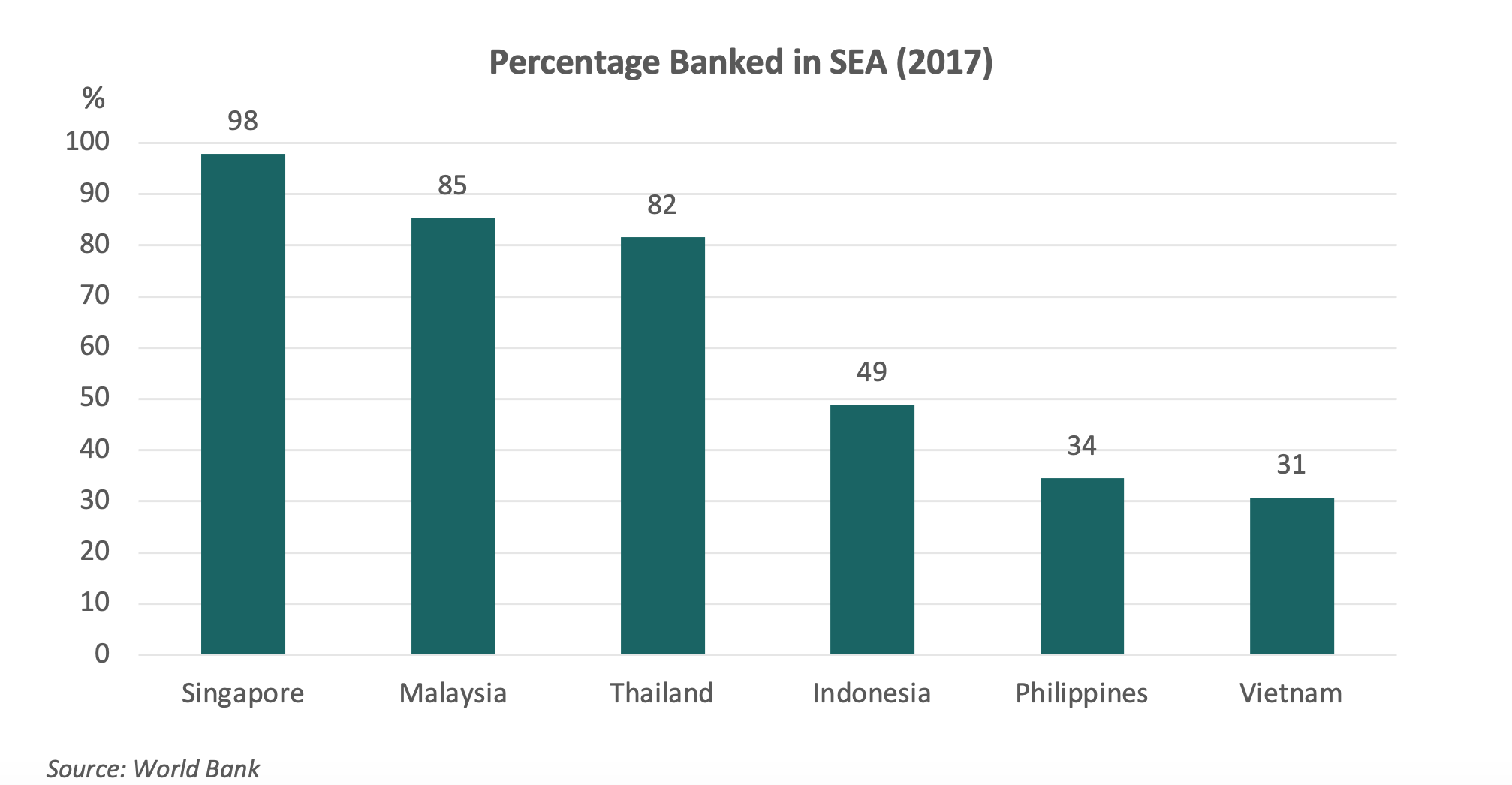

Household debt to GDP in Indonesia and the Philippines is low compared to the rest of the top SEA markets. One of the main reasons for this could be their relatively low banking penetration. According to World Bank data, the percentage banked (or the percentage of the population above the age of 15 that has a bank account) was around 49% and 34% respectively in Indonesia and the Philippines in 2017. Another market with relatively low banking penetration is Vietnam.

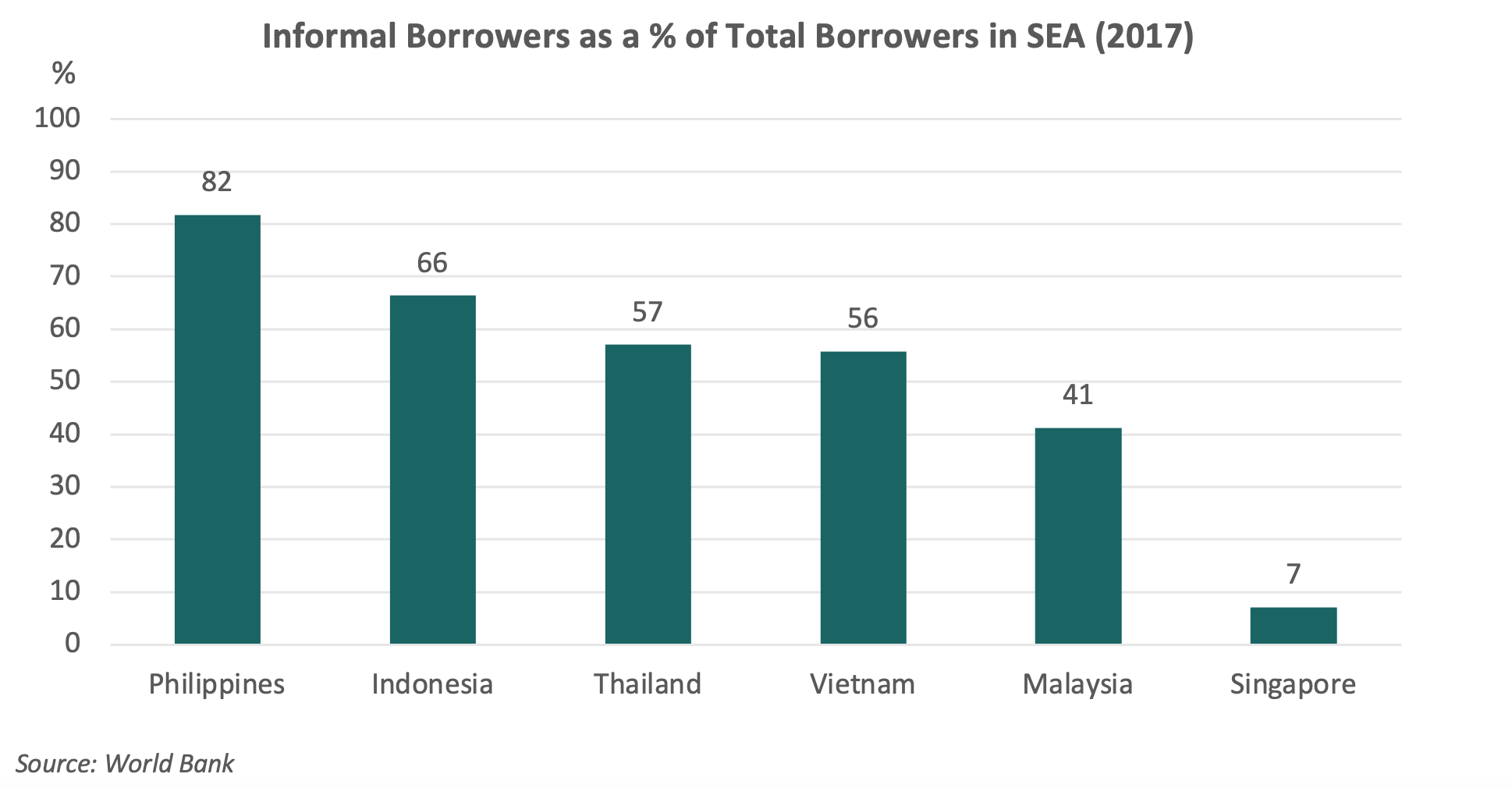

There is also a wider gap between formal and informal borrowings in SEA. According to World Bank data, around 67% of the Indonesians who borrowed money in 2017 did so from informal sources. This was as high as 82% in the Philippines, while in Thailand and Vietnam this was around 57% and 56% respectively.

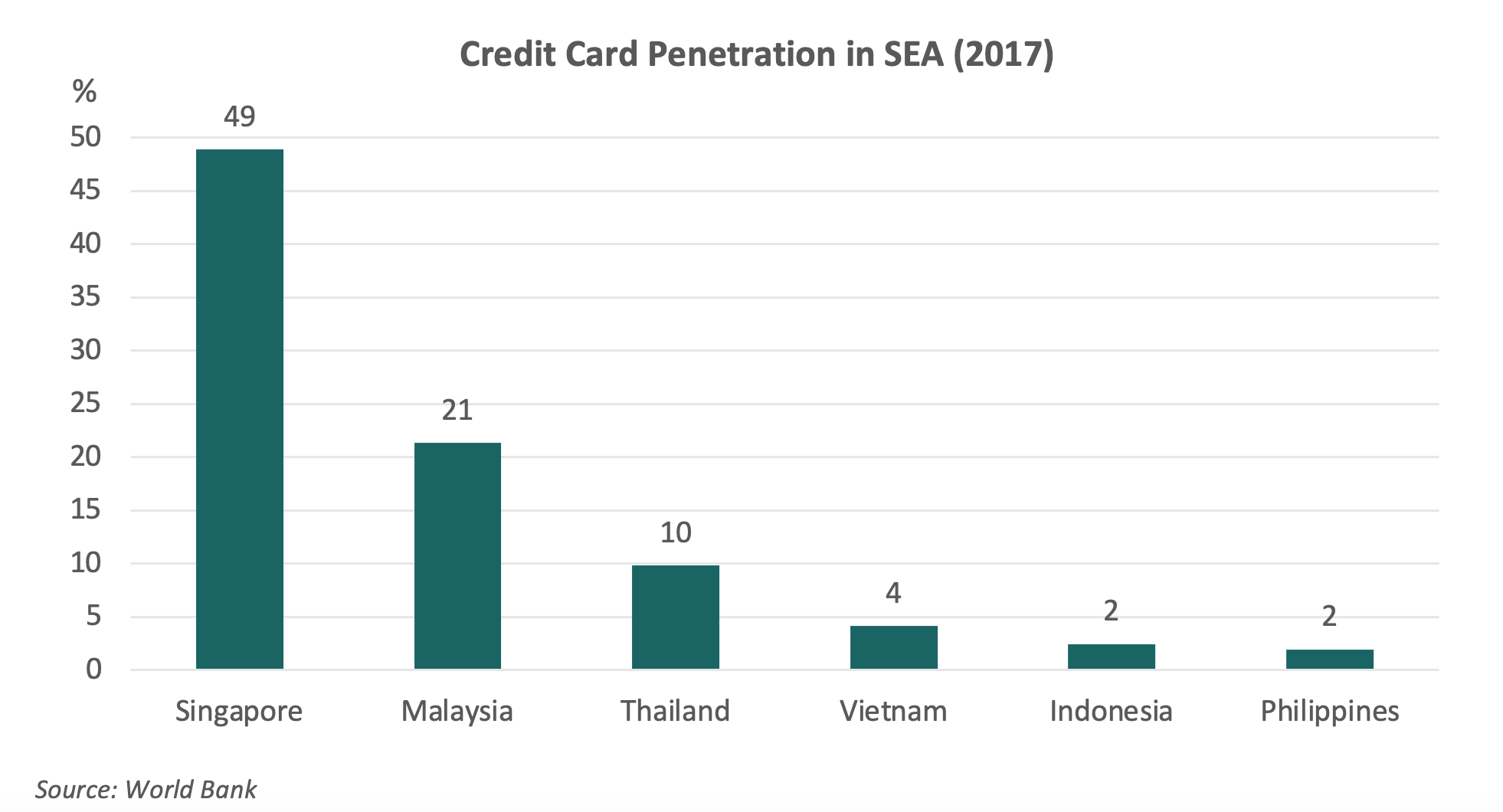

Credit card penetration in the SEA is also relatively low. Only Singapore and Malaysia had a credit card penetration rate of more than 10% in the region by 2017.

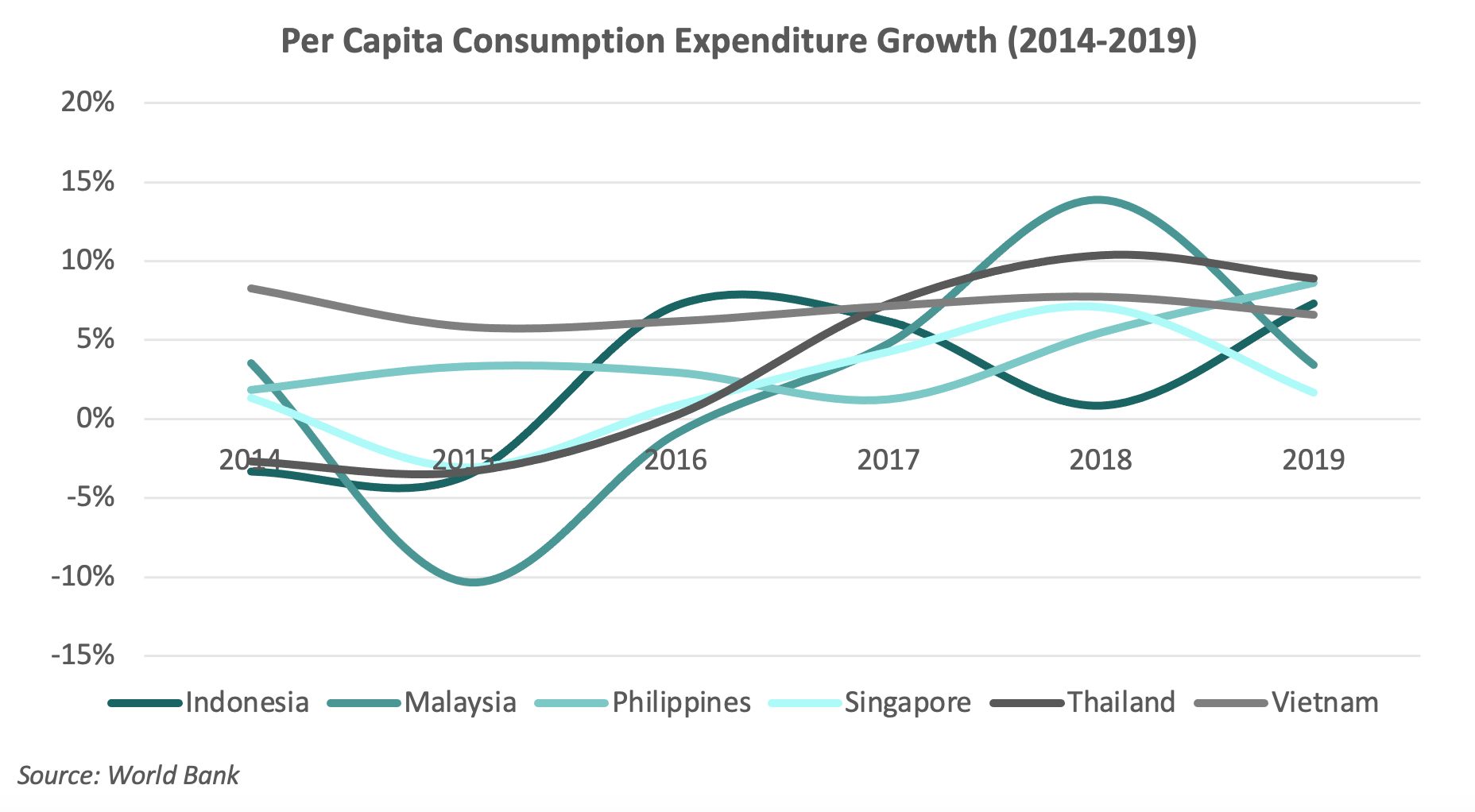

On the other hand, consumption expenditures across all major SEA markets have been growing at healthy 3-year CAGRs of 5%-10%. Higher consumption spending stimulates borrowing, ergo markets such as Indonesia, the Philippines, and Vietnam, which have relatively low access to formal credit, become attractive for alternative consumer lending businesses.

An opportunity for alternative lending to bridge the financing gap for SMEs

According to the Association of South East Asian Nations (ASEAN), SMEs contribute to around 30%-50% of the GDP of the member states. According to a 2017 World Bank report, the biggest obstacle for SMEs in SEA is access to finance. For instance, SMEs contribute to around 60% of Indonesia’s GDP, however, according to a 2019 report by the International Labour Organization, only 46% of the SMEs in Indonesia have been able to obtain a bank loan. There is an opportunity for alternative lending companies in SEA to bridge this financing gap.

In a recent survey by GrabFinance and Bloomberg among 600 SMEs in Singapore, Malaysia, Thailand, and the Philippines, around 29% of business owners said that they already use alternative financing, and around 58% of business owners said that they will turn to alternative financing over the next three years.

Singapore and Indonesia are the only SEA countries so far to regulate alternative lending

Singapore and Indonesia are the only SEA countries that currently have specific regulatory frameworks for the alternative lending industry. However, Singapore’s regulations on alternative lending are mostly limited to online crowdfunding operations (or in other words, online business lending/financing operations). The regulation does not specifically distinguish between online and offline consumer lending, and there are currently no specific regulations that govern P2P or marketplace consumer lending in Singapore.

In Indonesia, the situation is quite the opposite, where online lending laws are mostly applicable for P2P lending activities (both consumer and business lending). One of the key points to note is that under Indonesian regulations, online lenders are prohibited from providing on-balance sheet loans, meaning that loans must be funded only by third-parties (such as through loan underwritings, P2P financing, etc.).

In other SEA markets, existing regulations do not generally make a distinction between online and offline lending.

According to The Global Alternative Finance Benchmarking Report by the Cambridge Centre for Alternative Finance, around 64% of the alternative lending platforms in Indonesia believe that existing regulations on alternative lending are adequate and appropriate. However, in other SEA markets such as Singapore, the Philippines, and Malaysia, more than 80% of the alternative financing platforms believe that regulations are adequate and appropriate, suggesting that Indonesian regulations could be somewhat restrictive for alternative lending companies.

A highly fragmented market with a large number of small players; only a few notable established players

The alternative lending market in SEA is highly fragmented with the presence of a large number of small players. In Indonesia alone, there are more than 40 registered P2P lending platforms. Nevertheless, a few notable established players also exist.

The Indonesian company Akulaku, which operates the P2P lending platform Asetku, is the largest fintech lending company in SEA in terms of funds raised. However, in addition to its P2P lending business, Akulaku also operates an e-commerce platform. As of November 2020, Asetku has disbursed loans worth around $1.6bn (IDR 22trn) among over 3m borrowers.

Singapore-based company FinAccel, which operates the online point-of-sale financing platform, Kredivo (in Indonesia), is the largest pure-play alternative lending company in the SEA region by funds raised. As of November 2020, Kredivo has disbursed over 30m loans.

Funding Societies is another Singapore-based alternative lending company that has raised more than $100m in funding. Funding Societies also operates in Indonesia (under the name Modalku) and Malaysia. Funding Societies operates as a P2P lending marketplace for SMEs and has disbursed around 3.3m loans amounting to around $1.5bn as of November 2020.

Appendix

Akulaku

Akulaku operates Asetku, a P2P lending platform for individuals, and the Akulaku e-commerce platform, which allows consumers to pay for goods and services through instalment payments. As of November 2020, Asetku has disbursed loans amounting to IDR 22.0trn ($1.6bn) among more than 3m borrowers.

Akulaku was established in 2014. The company is headquartered in Indonesia, with operations in Malaysia, Vietnam, and the Philippines.

According to Crunchbase, Akulaku has raised a total of $218m in funding over 8 rounds. Akulaku’s latest funding round (series D) was in January 2019. Akulaku’s lead investors include Ant Group, FINUP, Qiming Venture Partners, Arbor Ventures, etc.

FinAccel

FinAccel is an online platform for point-of-sale financing. The company is based in Singapore but currently offers services only in Indonesia. The company was established in 2015.

FinAccel’s lending platform, Kredivo, allows online shoppers to apply for a loan through its mobile app and get approval within minutes if they qualify. Kredivo’s payments option is also integrated with a number of e-commerce firms, including Lazada and Shoppee, and food delivery start-ups in Indonesia, so users can quickly access the credit to purchase items and pay the app later.

As of November 2020, Kredivo has evaluated more than 3m applications and disbursed nearly 30m loans. FinAccel finances customer loans through bank credit. In the next three to four years, Kredivo aims to grow to 10 million users and expand to other Southeast Asian markets such as the Philippines, Thailand, and Vietnam.

According to Crunchbase, FinAccel has raised $120m in five funding rounds. Its investors include MDI Ventures, South Asia Growth Fund II (a joint venture between Mirae Asset and Naver), Square Peg Capital, Singtel Innov8, TMI (Telkomsel Indonesia), Cathay Innovation, Kejora-InterVest, Mirae Asset Securities, Reinventure, and DST Partners. FinAccel raised $90m in its last round of funding in December 2019, which valued the company at around $500m.

Funding Societies

Funding Societies (FS) is a P2P online lending marketplace for SMEs. FS claims to be the largest peer-to-peer lending platform in Southeast Asia. FS is based in Singapore, but the company also offers services in Indonesia (under the name Modalku) and Malaysia. FS was established in 2015.

FS offers term loans, working capital facilities, and invoice financing facilities for SMEs, while registered investors on the platform can choose to invest in any financial product of their choice. As of November 2020, FS has financed a total of around 3.3m loans worth SGD 1.9bn ($1.5bn). The current default rate is around 1.4%.

According to Crunchbase, FS has raised $113m in five funding rounds. Its lead investors include Softbank Ventures Asia and Sequoia Capital India. FS raised $70m in its latest funding round in 2020 (April-June).

KoinWorks

https://koinworks.com/super-app/en/

KoinWorks (KW) is a P2P financing platform in Indonesia. The company was established in 2016. According to its website, KW’s financial platforms have more than 300,000 users.

KW offers the following products: 1) KoinP2P – a P2P lending platform for Indonesians, 2) KoinBisnis – a P2P financing platform for SMEs, 3) KoinRobo – a Robo-advisory service for investors, 4) KoinGaji – a salary advance solution for employers, and 5) KoinGold – an online platform for buying and selling or investing in gold.

As per Crunchbase, KW has raised a total of USD 62m in funding over 5 rounds. KW’s lead investors include Triodos Bank Germany, Quona Capital, Saison Capital, and EV Growth. KW’s latest funding round was in April 2020.

Validus Capital

Validus Capital (Validus) claims to be the leading P2P lending platform for SMEs in Singapore. Validus was established in 2015.

Validus offers three main financing products for SMEs, namely Invoice Financing, Purchase Order Financing, and Working Capital Loans. According to Vikas Nahata, the Co-founder of Validus, the company’s current focus will be to develop strong teams and a deep-rooted presence in each of the markets it operates in, to become the #1 platform of choice for SMEs and investors. In addition to Singapore, the company also provides services in Indonesia and Vietnam.

According to Crunchbase, Validus has raised $50m in five funding rounds. Validus’ investors include Vertex Ventures, FMO, and K3 Ventures. Validus raised $20m in its latest funding round in May 2020.

Aspire

Aspire provides digital banking and lending solutions for SMEs in Singapore. Aspire was founded in 2018 and is currently a fully owned subsidiary of US-based Aspire Financial Technologies Holdings Inc.

Aspire primarily offers digital banking solutions for SMEs through its Aspire Account. SMEs can use the account to transfer and receive money. In addition to this, Aspire provides working lines of credit for SMEs. Aspire also provides customised financing solutions to companies that have annual revenue of more than SGD2m.

Aspire claims to have more than 100,000 SMEs on board. Aspire’s website suggests that they also have teams in Vietnam, Indonesia, and Thailand. However, there is no further evidence that the company is operational in these markets.

According to Crunchbase, Aspire has raised $42m in three rounds of funding. Aspire’s investors include the Pioneer Fund, Arc Labs, Hummingbird Ventures, Beacon Venture Capital, Picus Capital, Y Combinator, and MassMutual Ventures Southeast Asia. Aspire raised around $33m in its latest funding round in August 2019.

Credit Culture

Credit Culture (CC) is an online personal loan platform founded by a team of veteran ex-bankers in 2016. The company claims to be the first to provide digital solutions for personal loans in Singapore and is one of the six companies selected by the Singapore Ministry of Law to pilot new business models for money lending in Singapore.

CC raised SGD 40m ($30m) from Malaysia’s RCE Capital Berhad in January 2019. This is the company’s sole funding round. In an interview with TechCrunch last year, a CC representative said that the company is open to exploring various options for regional expansions and has plans to expand to other SEA countries like the Philippines and Indonesia.

First Circle

First Circle (FC) is a Philippines-based online financing platform for SMEs. FC was launched in 2016. FC specialises in offering short-term business loans, but also offers Invoice Financing and Purchase Order Financing services.

According to Crunchbase, FC has raised a total of $29m in funding over 5 rounds. FC’s lead investors include Accion Venture Lab, Venturra Capital, Key Capital, and Betafabrik. FC’s latest funding round (Series A) was in October 2018.

UangMe

UangMe is an Indonesia-based P2P financing platform for individuals. As of November 2020, UangMe has disbursed loans worth IRD 3.9trn ($0.3bn) among 731K borrowers. There are also around 4m investors registered on the platform. As per Tracxn, UangMe raised $24m in a Series B funding round from Gobi Partners and Cheetah Mobile in September 2019.

Investree

Investree is an Indonesia-based P2P financing platform for SMEs. Investree was established in 2015. As of November 2020, Investree has disbursed loans amounting to IDR 5.4trn ($0.4bn) among 1,500+ borrowers. Investree offers several loan products such as Working Capital Term Loans, Invoice Financing, Buyer Financing, and Online Seller Financing.

According to Crunchbase, Investree has raised a total of $24m in funding over 5 rounds. Investree’s lead investors include SBI Group and Kejora Ventures. Investree’s latest funding round (Series C) was in April 2020.

Investree plans to introduce new services such as electronic invoicing and is also in collaboration with Mbiz to provide e-procurement services. Further, the company is already working to obtain licences to operate in Thailand and the Philippines, where it has set up joint ventures with local companies 2C2P and Filinvest Development Corporation respectively.

ADDX is your entry to private market investing. It is a proprietary platform that lets you invest from USD 10,000 in unicorns, pre-IPO companies, hedge funds, and other opportunities that traditionally require millions or more to enter. ADDX is regulated by the Monetary Authority of Singapore (MAS) and is open to all non-US accredited and institutional investors.