The first half of 2022 was challenging for investors across various asset classes. Within the span of a few months, we saw the US Federal Reserve raising its benchmark interest rates aggressively in an attempt to bring down inflation, the Ukraine crisis exacerbating global supply chain disruptions, and China’s economic growth slowing rapidly as its government tried to control the domestic Covid-19 outbreak. It almost felt like there was nowhere to hide from this perfect economic storm.

Against the backdrop of this uncertainty, we previously explored how the private markets could be more resilient than public markets in our earlier ADDX Insights: “Are the private markets more resilient than public markets?”. Private markets have demonstrated their ability to outperform public markets historically. One important reason for this is that private market assets are not marked to market in the way public market assets are. This means fund managers focused on private markets have more freedom to hold on to investments based on their long-term conviction in the prospects of the underlying companies or assets. Private markets also offer the additional advantage of having a low correlation with public markets and therefore providing diversification as one constructs a resilient portfolio.

It is therefore noteworthy that the Government of Singapore Investment Corporation (GIC) increased its exposure to private equity to 17% as at 31 March 2022, from 15% the previous year. In explaining its decision for the shift in portfolio allocation, GIC wrote: “Within equities, we have increased our allocation to certain high-growth asset classes, such as private equity, that can provide returns that keep pace with elevated inflation.”

As the economic outlook darkens and recession risks rise, are private markets proving to be where the better performance lies?

A recent detailed analysis from Bain & Company suggests that private equity investors may have less to fear from a recession. This is because inflation-recession cycles tend to be relatively short-lived, and the long term outlook for private equity remains strong. Private equity funds have US$3.6 trillion in dry powder, or undeployed capital, positioning them well to seize opportunities as the economy recovers from the downturn.

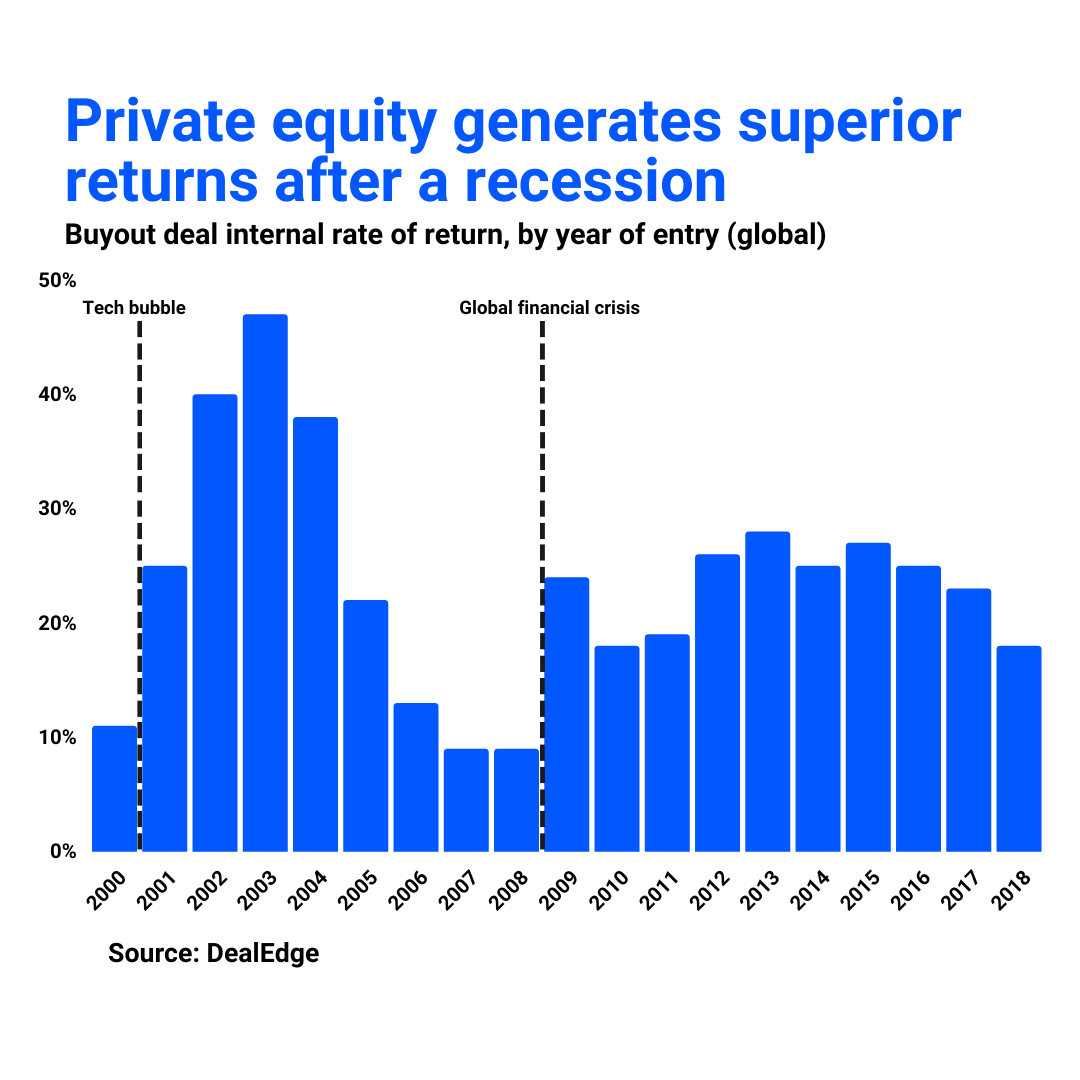

But here’s the critical point: post-recession opportunities have historically shown superior returns. Research from Bain showed that the internal rate of return (IRR) from investments made during recovery years has consistently exceeded long-term averages. For example, following the dot-com bubble burst, buyout firms posted a median IRR of 25% in 2001, 40% in 2002, and 47% in 2003. There was a smaller but still significant boost after the global financial crisis of 2008.

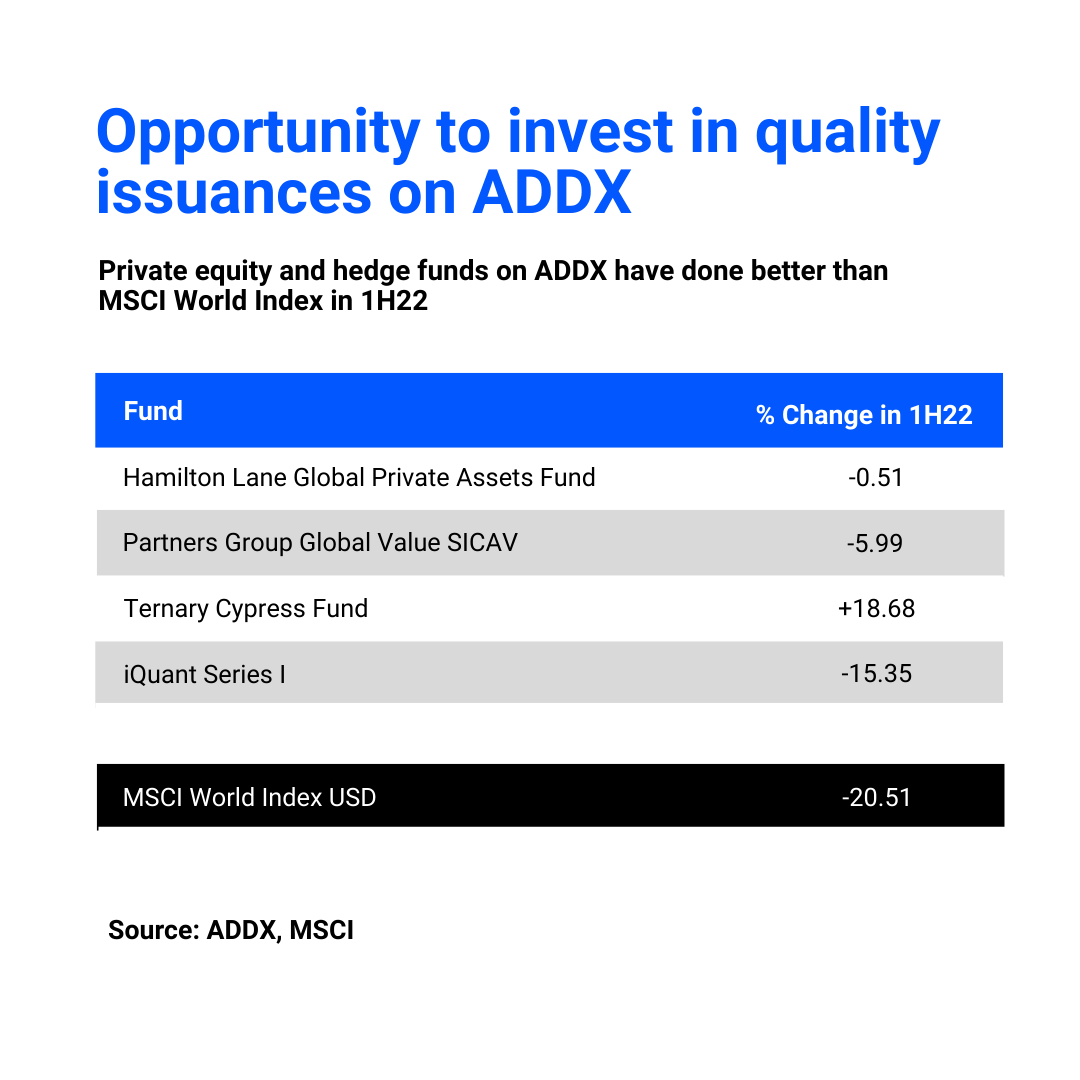

The outperformance of hedge funds is also evident amidst ongoing market volatility. Preqin estimates that hedge funds generated a net return of negative 7.95% in 2Q 2022. This would bring its cumulative decline in 1H 2022 to about 9%, following a 1.47% decline in its hedge fund benchmark in 1Q 2022. This compares to a 20.51% fall in the MSCI World index over the first half of this year.

How have private equity and hedge funds on ADDX performed?

In the first half of 2022, we continued to make noteworthy strides in the growth journey of ADDX. This is reflected in the robust pipeline of new issuances which offer investors a steady supply of high-quality opportunities. In addition, the performance of several private equity funds and hedge funds listed on ADDX have outperformed the MSCI World Index, a commonly used global public equity index.

This is demonstrated by the robust performance of the Hamilton Lane Global Private Assets Fund (Token Ticker: HAML), which marked the first time private markets investment firm Hamilton Lane has tokenised a fund. Nasdaq-listed Hamilton Lane is one of the world’s largest investors and allocators of capital to the private markets and has a highly selective and robust diligence process.

The Hamilton Lane Global Private Assets Fund has achieved strong risk-adjusted returns with an annualized return since inception of 13.91%. Against the backdrop of a weaker economic environment, the Fund saw a return of -0.51% in the first half of 2022. This was a significantly better performance when compared with the 20.51% decline in the MSCI World Index over the same period.

Investors in the fund can gain access to Hamilton Lane’s relationships with reputable general partners around the world. Its private markets portfolio across direct private equity, direct private debt and secondaries is diversified by investment type, geography, industry, deal size, strategy and general partner.

The Hamilton Lane Global Private Assets Fund is one of the several open-end private equity funds listed on ADDX. Issued by another major global player in the private markets, the Partners Group Global Value SICAV (Token Ticker: PGGV) is an open-end private equity fund that offers immediate exposure to a globally diversified private equity portfolio with no J-curve effect. This would eliminate the tendency of some private equity funds to post negative returns at the onset of investments due to investment costs, management fees and the time needed for an investment to mature.

As the fund manager, Partners Group sees its emphasis on operational excellence as a strong competitive advantage. It adopts a dynamic asset allocation strategy through investments in directs, primaries and secondaries.

Since the fund’s launch, it has achieved a historical outperformance against public markets at significantly lower volatility. This was the case once again in the first half of 2022, when the fund saw a return of -5.99%, outperforming the MSCI World Index.

Outside of open-end private equity funds, several hedge funds listed on ADDX also performed well relative to public equity indices. The Ternary Cypress Fund is a hedge fund that focuses on scarce, real assets like nuclear, oil tankers and specialty engineering. It adopts an asset-based approach towards investing, with investments made primarily in the debt and equity of small and mid-cap public companies with distressed valuations that have strong asset-backed balance sheets.

The fund aims to deliver superior returns through investments in publicly-listed securities and targets to grow invested capital by 300% over a three- to five-year investment period. The significant gains made by Ternary Cypress Fund continued in the first half of 2022, when it saw a positive return of 18.68%. This hinged on its strategy to invest in sectors that typically benefit from favourable supply-demand dynamics, with potential catalysts that can propel prices upwards, particularly in an inflationary environment.

Another hedge fund listed on ADDX is the iQUANT Series I Fund, a feeder fund into the top-ranked global macro hedge fund Quantedge Global Fund (QGF). QGF adopts a strategy of ultra-diversification, dynamic asset allocation and constant total risk to extract market premiums within multiple asset classes and geographical regions. This has helped the iQUANT Series I Fund achieve better returns compared to the MSCI World Index, with a return of -15.35% in the first half of 2022. Annualised returns of QGF since its inception in 2006 stand at 21% at the end of 2H2022.

Expertise to spot good opportunities

The outperformance of private markets when compared with public markets does not suggest that there is anything easy about managing investments through this period of economic turbulence. As Bain noted in its Global Private Equity Report 2022, private equity fund managers have had to make several adjustments to due diligence in this time of inflation.

Likewise, the outperformance of funds on the ADDX platform did not come about by chance. We actively source opportunities through decades of investment experience and established networks.

The initial screening process for listings may entail:

- Track record: We evaluate the reputation of the issuer, its historical performance compared to the industry average, as well as its growth prospects.

- Audited financial statements: Our team assesses the financials of the issuer, evaluating metrics such as its profitability, gearing level and cash position.

- Background checks: We conduct due diligence on the leadership team and assess the board of directors.

- General market trends: The team curates investment listings that are in line with the current macroeconomic environment and latest market trends.

Next, the issuance would go through a secondary screening, where the following would be evaluated:

- Corporate governance: We assess the issuer's business practices and its offer documents.

- Compliance: We assess the deal terms to ensure that it abides by our listing requirements.

Our listing committee comprising industry veterans with decades of financial experience assesses the offering only after all the above criteria are met. It is then offered to investors on ADDX for primary subscription.

Private markets have demonstrated once again in the first half of 2022 that they are less volatile and less vulnerable to short-term noise than the public markets. The resilience of private markets can help to reduce heart-stopping ups and downs typical of a public stock exchange. In addition, a rigorous selection process will produce a shelf of high-quality products that investors can turn to when building a solid and robust portfolio to weather the storm.

This research is commissioned by ADDX in collaboration with Canopy Research, a bespoke insights provider by Beansprout dedicated to guiding investors along their financial journey. Beansprout is a next-generation investment advisory platform licensed by the MAS.

This article is for general informational purposes only and has not been independently verified to ensure its accuracy and fairness. This article does not constitute any advice or recommendation from ADDX or ICHX Tech Pte. Ltd. (“ICHX”) or any of its affiliates. Please consult your own professional advisors about the suitability of any investment product/securities/ instruments for your investment objectives, financial situation and particular needs. No representation, warranty or other assurances of any kind, expressed or implied, is made with respect to the accuracy, completeness, adequacy, reliability validity or availability of any information in this article. Under no circumstance shall ADDX or ICHX have any liability to the reader for any loss or damage of any kind incurred as a result of the use or reliance on any information provided in this article. This article may not be modified, reproduced, copied, distributed, in whole or in part and no commercial use or benefit may be derived from this article without the prior written permission of ADDX and ICHX. ADDX and ICHX reserve all rights to this article.